Binance Insurance Fund: Fraud with the shutdown of the futures platform on May 19 (technical analysis and evidence)

We recommend you to read:- Investigation by Coalexander.com: Trading Operations of the Binance Insurance Fund

Binance is a manipulation and casino in the cryptocurrency market, no less - exceptional fraud, by any means, under any pretext. Binance steals not only investors and traders (like their clone exchange FTX), but also countries, states and financial regulators and it does not matter where it is - USA, China, Malaysia, Australia, Thailand, India almost anywhere in the world Binance activities are illegal, unregulated and harm not only the economy of the country, but also the financial situation of ordinary citizens - even in the "offshore region, the Cayman Islands". The falsification of volumes on the exchange (as well as on FTX) is fantastic, but how else can you call yourself "the biggest and №1 in the world", if only by fraud and deception? You can't.

Does Binance worry about its future? Apparently, yes. Otherwise, why would they hide the real beneficiary Guangying Chen (Heina Chen) and expose a clone with Canadian citizenship or Changpeng Zhao, who in turn is gradually looking for a replacement for this "rotten place." After all, they want to throw off all responsibility for a mountain of financial crimes as soon as possible. Not for nothing, exchange-casino FTX (Sam Bankman-Fried, Alameda Research cryptocurrency fund) publicly (allegedly) disowned Binance. Apparently, the Binance-FTX-Tether cartel is preparing a new springboard for its criminal activities.

One of the favorite technical tricks of Binance casino, and they have a lot of such tricks, do not forget the regular fraud with FTX BULL / BEAR (UP/DOWN) tokens - to shut down the spot or futures platform at the right moment. Thus, we lost money on September 21, 2018, over 86.000 USDT, thus on May 19, 2021 a huge number of traders lost their money (instead of fixing profits, they lost money - even though they chose the right position). Such incidents are extremely numerous, they occur regularly and on a regular basis.

A group of traders we wrote about in the article Binance Users from Australia are considering the possibility of class action over Binance failures were able to attract technical experts to their problem, who proved by technical analysis that such "technical failures, as the shutdown of Binance platform is extremely profitable for the casino, and furthermore, if the platform did not shut down trading, it would be bankrupt", that is - Binance purposely and deliberately restricts the functionality of traders in peak situations and directly steals from traders. These are exceptional moments of public manipulation of the market and its functionality, such in real life, even casinos in Macau or Vegas do not allow themselves. Interestingly, similar technical tricks are used by FTX casino - the same fraud in its purest form.

The question that arises in this investigation is. Why? Why does Binance commit fraud in such a way? Wouldn't it be easier to "accrue profit to traders", because sooner or later they will lose it? The answer is very simple - the Binance casino does not have the liquidity in the necessary amount, its trading volumes are rigged in an extremely large amount (hundreds, thousands of times), and there is no money to pay out such "winnings" to the traders. It's easier to steal not only their "winnings", but also their operating capital. Binance casino is nothing on the cryptocurrency market, just like FTX casino. In parallel, the organizers of Binance fill their pockets with traders' money, who have no idea what an "offshore hole" they got into.

We publish a technical investigationby: Carol Alexander (Professor of Finance at the University of Sussex Business School and Visiting Professor at the HSBC Business School, Peking University):

Binance’s Insurance Fund

How insufficient insurance funds might explain the outage of Binance’s futures platform on May 19 and the potentially toxic relationship between Binance and Tether.

Had Binance’s futures platform continued to operate normally, professional traders could have realised very substantial gains on positions where counterparties had been liquidated, and these gains should have been financed from Binance’s insurance fund. However, there is considerable doubt as to whether the value of the fund could have covered such extensive potential claims, so the outage of the futures platform was very convenient for Binance. The winning counterparties were unable to realise their gains resulting from 30% price fall, and once trading resumed the gains had been wiped out.

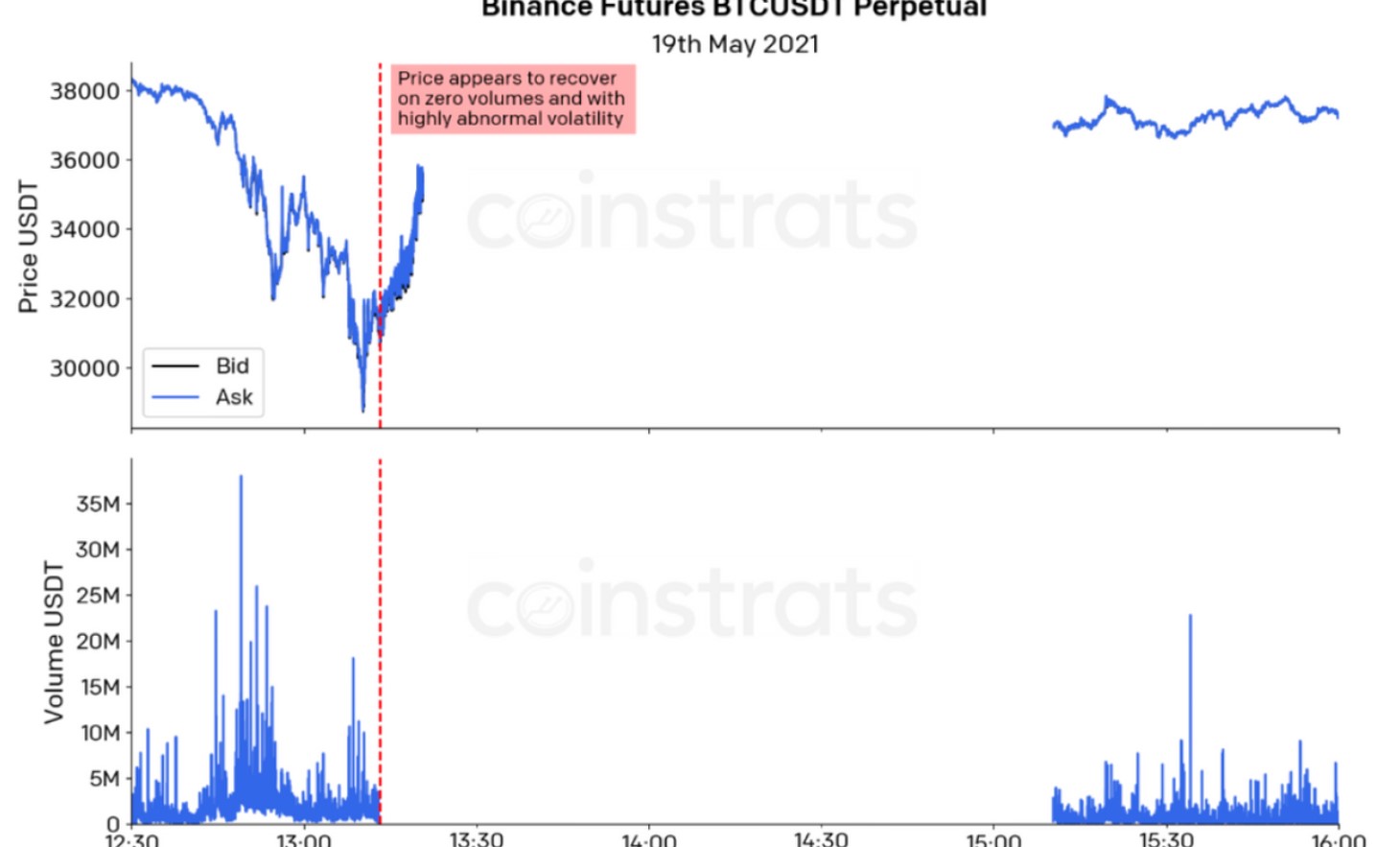

On May 19 at lot of retail investors lost a lot of money when bitcoin fell from $38,000 to less than $30,000 in the space of 30 minutes. As ever, other crypto assets followed suit. At the height of the crash, between 12:40 and 13:10 UTC, there are video reports claiming that the Binance futures platform developed some sort of bug making it impossible to add collateral to losing long positions. As the price started to recover, one would expect a lot of winning short positions to close out, to realise their gains.

The data depicted in Figure 1 shows how the price fall on the BTCUSDT perpetual apparently precipitated a strong but highly volatile recovery – but it was on zero reported trading volume. So the winning shorts were unable to close their positions. Then, shortly before 13:30 the entire platform crashed. It re-opened soon after 15:00 UTC by which time bitcoin and other crypto prices had recovered to pre-crash levels and the short positions were no longer in-the-money.

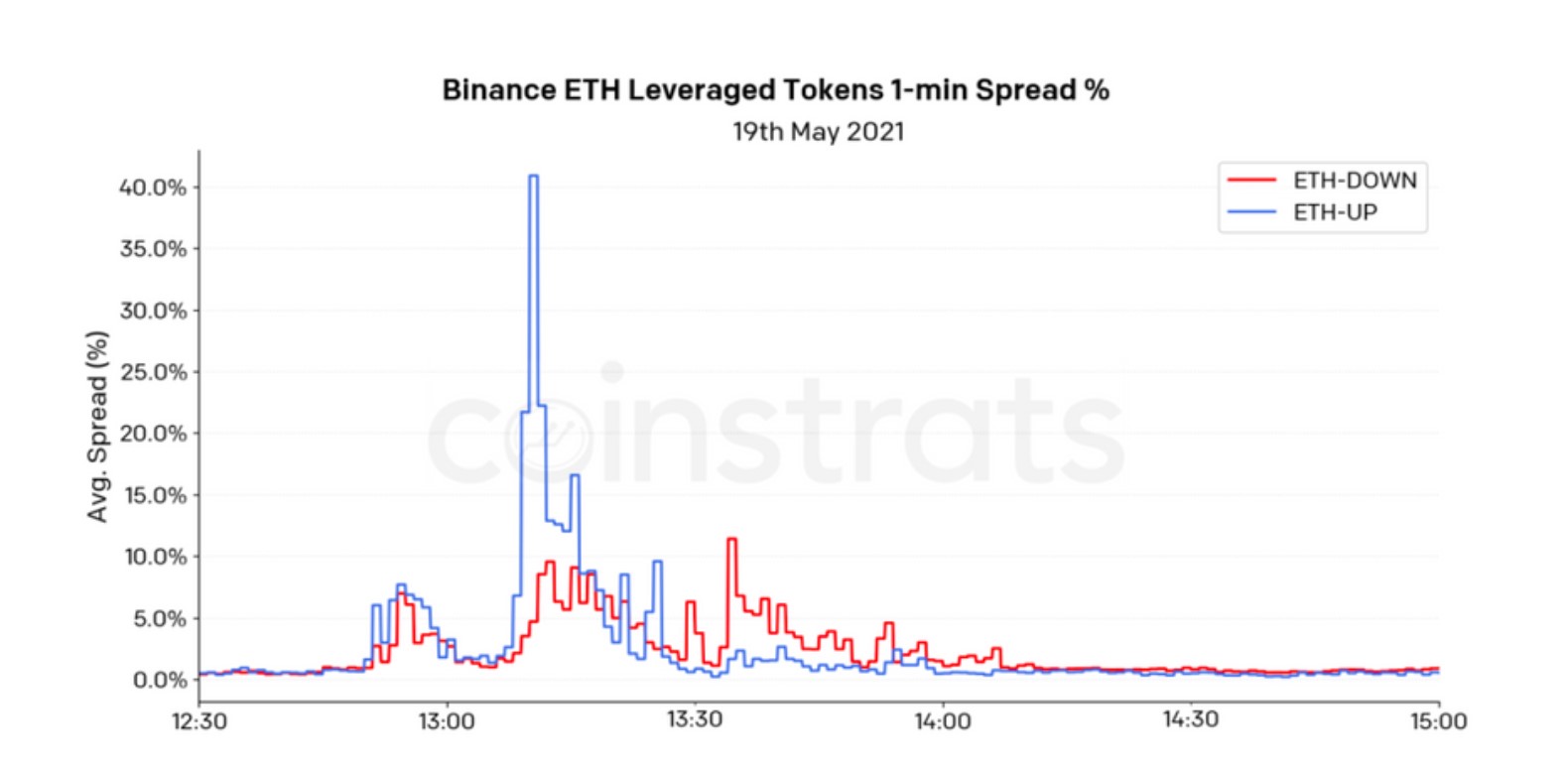

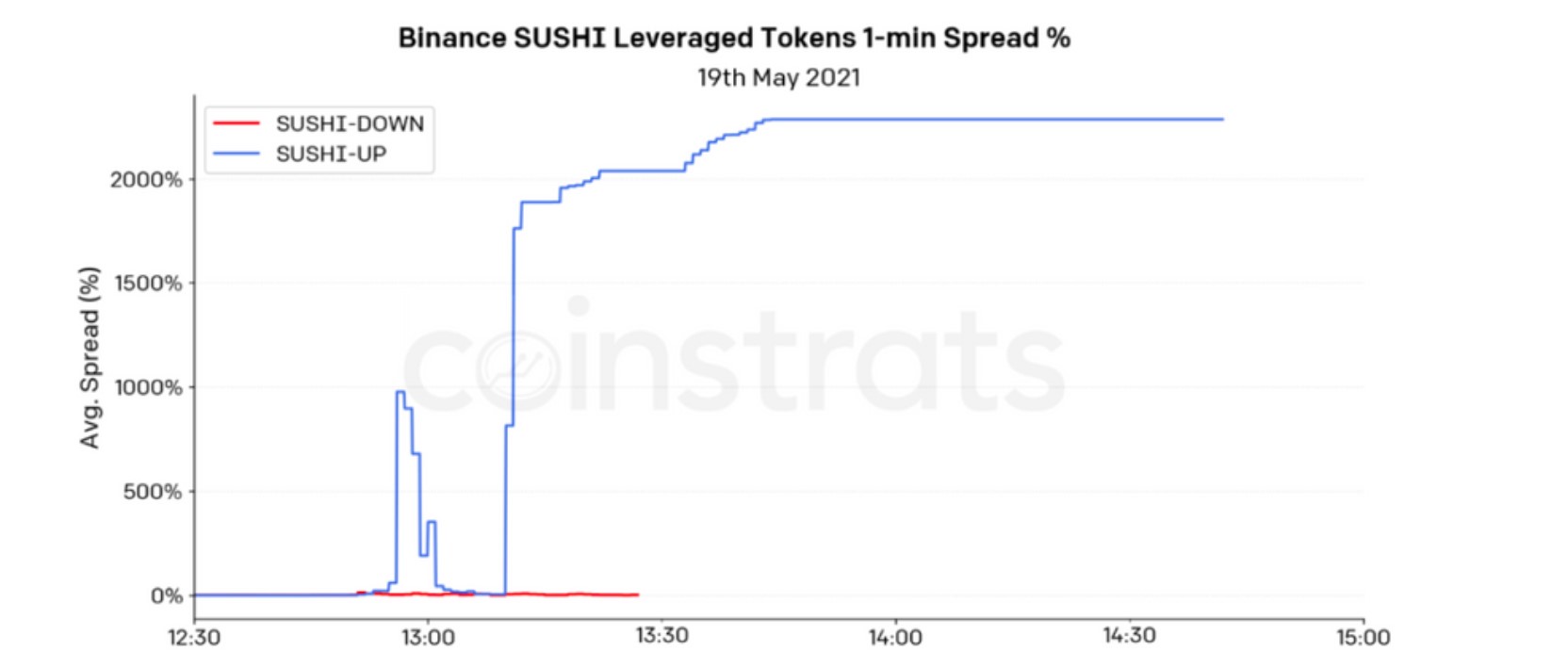

At the same time on May 19, positions on leveraged tokens recorded huge losses instead of gains. For instance, Figure 2 shows the spreads on two different UP and DOWN tokens between 12:30 and 15:00 UTC on 19 May. The upper part of Figure 2exhibits the ETH UP and DOWN token spreads and the lower part shows the SUSHI UP and DOWN token spreads. As the entire futures platform crashed, the ETH UP token spread briefly reached 40%. The SUSHI UP token widened first to 1000% then up to 2000% and it stayed there for the next few hours. The leverage also increased to 50X – way outside the stated (1.25, 4) leverage range and, as a result, all long SUSHI UP positions were wiped out.

The events of May 19 have been covered extensively by the WSJ and numerous other press reports. As Adam Samson and Joshua Oliver explain in their 27 July FT article about Binance on 19 May, those using leverage found positions automatically liquidated as the crypto price drop wiped out all the collateral in their margin accounts before they could transfer extra funds onto the exchanges. This blog post examines another side of the story – the actual value of Binance’s insurance fund and its ability to meet the potential pay-outs on 19 May, had the platform not been closed. I no longer believe the figures that Binance shows on its website for its insurance funds, nor their liquidation reports, and I maintain that a figure of only 3 million USDT for the BTC/ETH insurance fund pay-out on May 19 is grossly inconsistent with the actual number of liquidations on BTC and ETH products on that day. In fact, if the futures platform had not closed, I believe that Binance would have had to subsidise its insurance fund by a billion USDT or more.

Historical Data on Liquidations

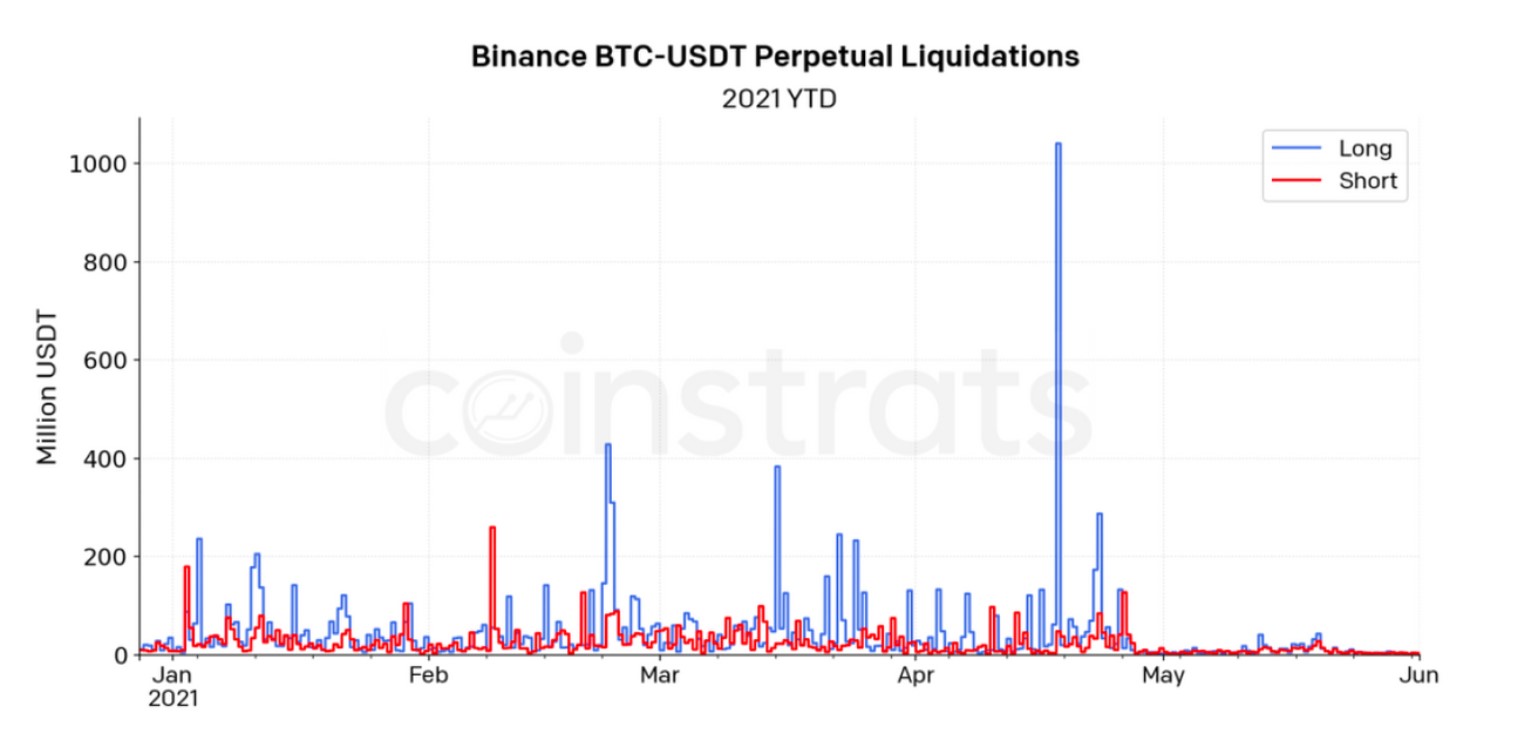

Automatic and immediate liquidations are a feature of all the unregulated crypto derivatives exchanges which (characteristically flaunting the regulations that took years to develop in traditional markets) operate as their own central counter party (CCP) clearing house without external supervision. Most exchanges report data on liquidations to Bybt and these frequently run to hundreds of millions of dollars, as illustrated in Figure 3.

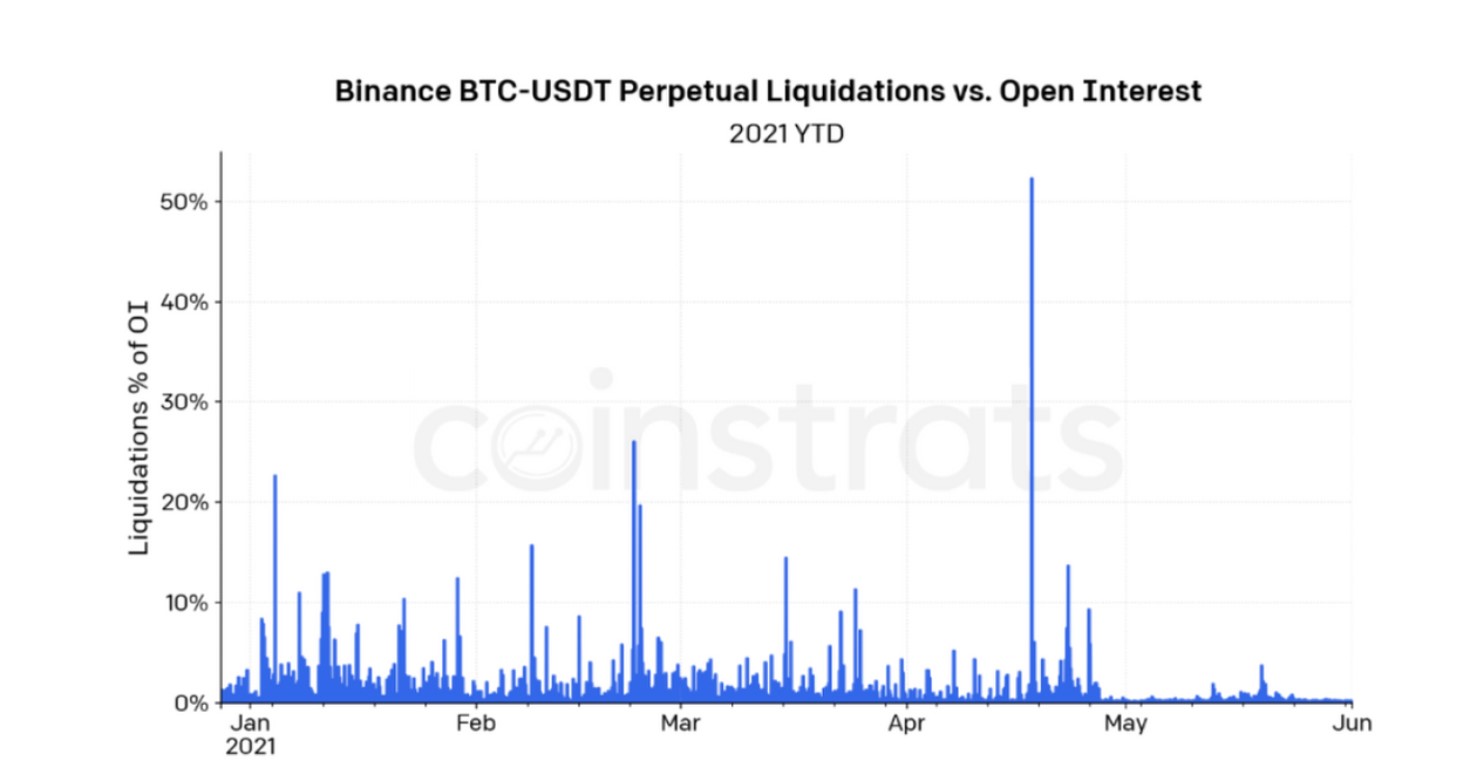

Historically, the BTCUSDT perpetual is the largest contract on Binance by both trading volume and open interest. Figure 4 shows the long and short liquidations on the BTCUSDT perpetual at a 4-hourly frequency from the start of this year until 31 May. On 18 April when the bitcoin price fell by 8.7% between 00:00 and 04:00 UTC, long positions worth over 1 billion USDT were liquidated. Figure 5 shows the same data, as a percentage of open interest. On 18 April over 50% of the open interest on the BTCUSDT perpetual was wiped out through long liquidations.

What is striking about both Figures 4 and 5 is that the data change dramatically after the beginning of May. However, there has been no change to Binance’s clearing methodology, and both open interest and trading volume data seem accurate. The lack of liquidations is simply inconsistent with previously reported data and that is why I do not believe in these figures.

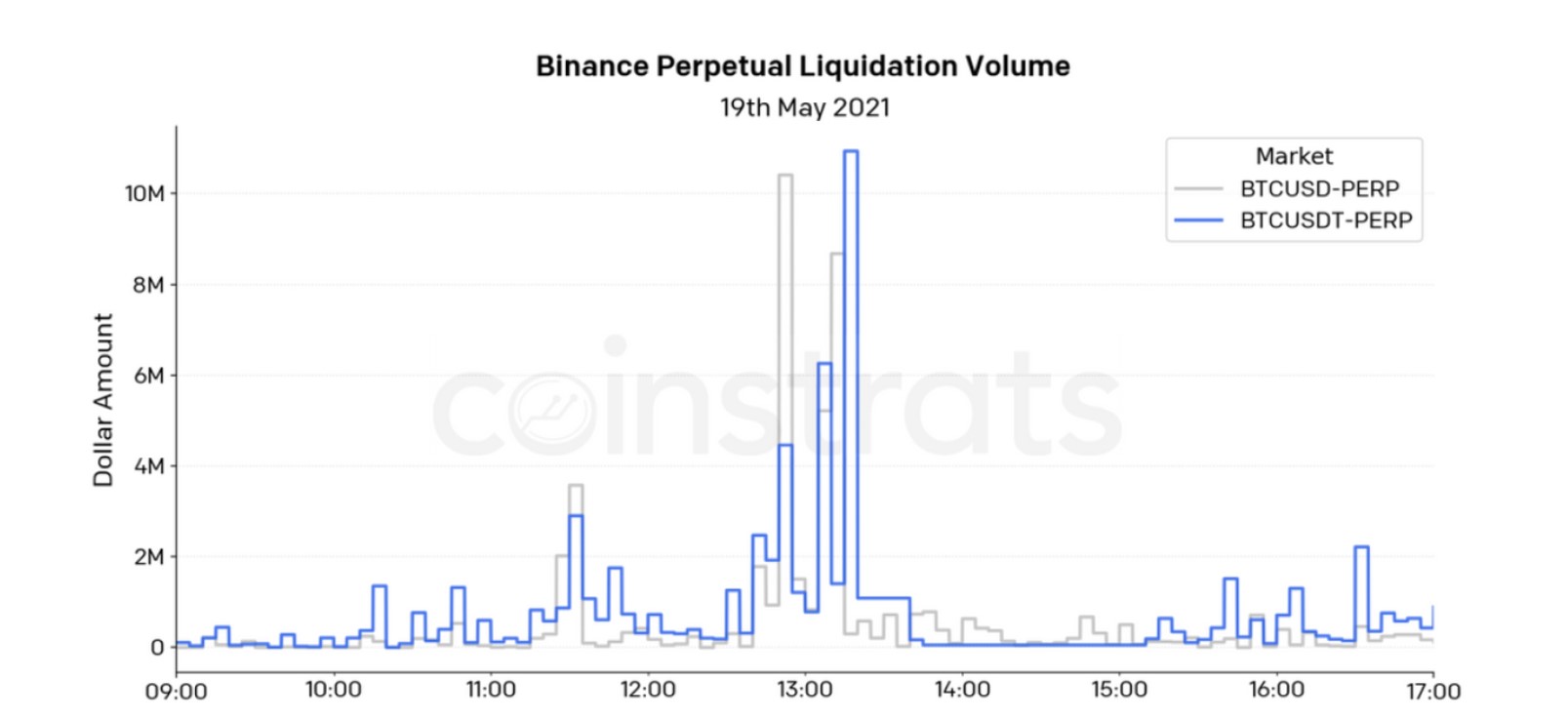

On 19 May the BTCUSDT price fell by more than 30% yet Binance reported liquidations of merely 24 million USDT – see Figure 6. But I do not believe these data because:

1. On 19 May other exchanges together reported $8.6 billion liquidations to Bybt;

2. Binance is larger than all the other exchanges combined;

3. The trading volume on Binance’s BTCUSDT perpetual alone reached almost $100 billion on May 19;

4. There are numerous press reports of huge losses experienced through liquidations on Binance on 19 May.

How Binance’s Insurance Fund Works

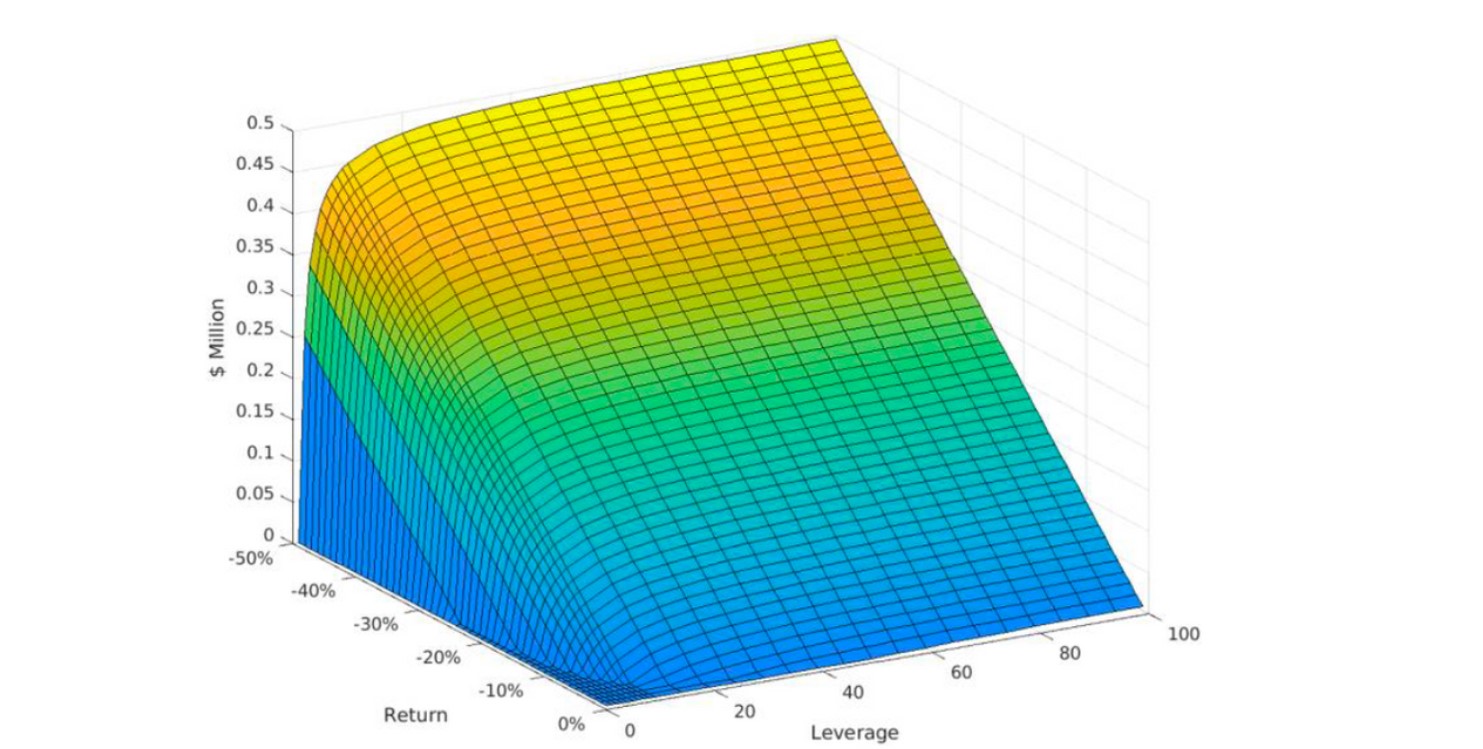

Let’s examine how the insurance fund works. Here is a simple spreadsheet based on the formula I derive below, which is used to plot Figure 7. First, look at the example in its caption. The data were coded using the simple formula displayed below, based on the notation N for notional ($1 million in the figure), for different leverage, L and return, R. The caption example assumes leverage is 20X and the return is -10%. Initial margin rates are 1/leverage and maintenance margin rates are half the initial margin rate. So, a maintenance margin is (2L)-1 N = $25,000 for a long position of notional amount N = $1m with leverage L = 20.

Let us call the long position holder Alice. Her return is based on the notional amount N. That is, when the return is R Alice’s profit is RN and her loss is -RN. For instance, with a return of -1% on a notional N = $1 million, she loses 1% of $1m = $10,000. At this point her maintenance margin actually changes – in fact, to be really precise, her ‘liquidation level’ changes. The liquidation level is calculated using a very complex formula with many parameters. But it is always very close to the maintenance margin, so I shall continue without adding this further level of complexity.

Similarly, Binance use a mark price for liquidations, but again it is more complex than it needs to be – other exchanges like Bybit use much less complex formulae for liquidation prices and market prices. The aim of this blog is to get a back-of-the-envelope idea of the potential claims on Binance’s insurance fund, so I’m not going to make this more complex than necessary.

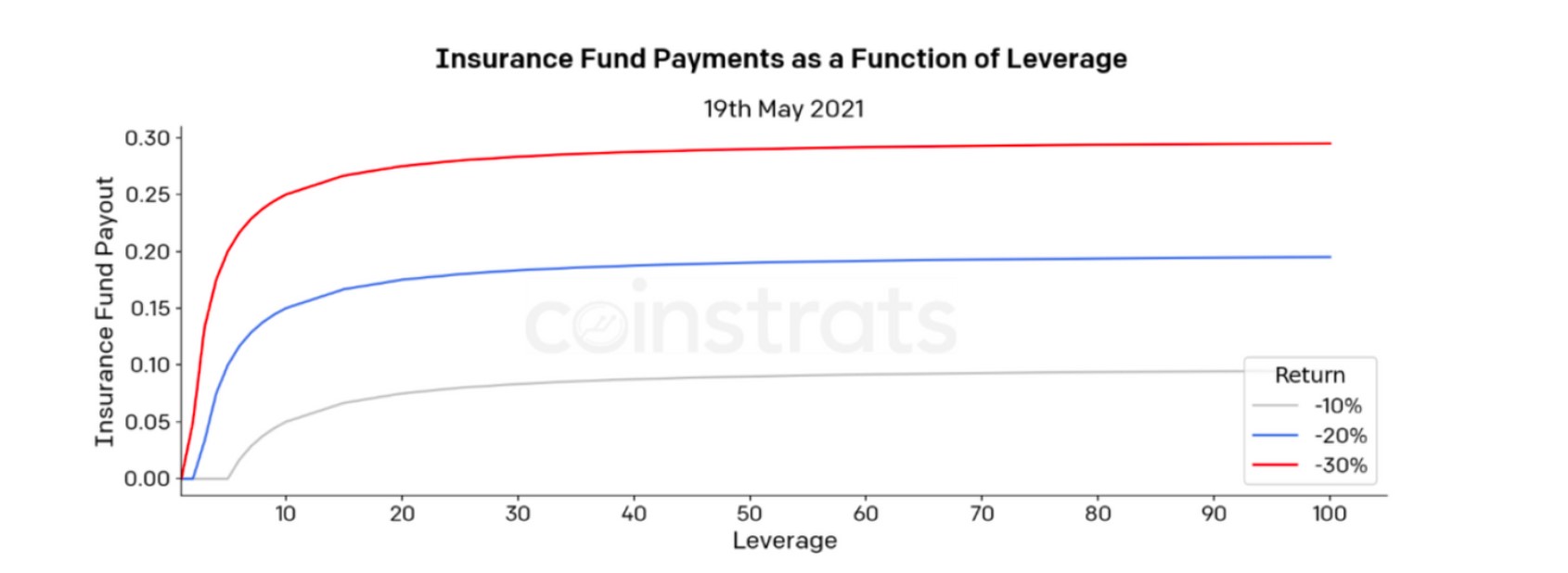

Ignoring extra complexities such as liquidation and mark price calculations, Alice’s position will be liquidated if the loss exceeds the maintenance margin. That is, if -RN > 1/(2L) x N, that is if -R > 1/(2L). Thus, the insurance fund pay-out to the short counterparty (call him Bob), if Bob decides to close the position immediately, is Insurance Pay-Out = Max {-[R + 1/(2L)]N,0}.

To illustrate this formula with and for particular values of N and R, Figure 8 shows slices through the surface of Figure 7 at returns of -10% (red), -20% (blue) and -30% (black) with N = 1. For different values of N, we just multiply the result by that value. For example:

- On a return of -20% a liquidated position of 1 billion USDT with a leverage of 100X would require an insurance fund pay-out of [0.2 – 1/200] = 0.195 billion USDT;

- On a return of -30% a liquidated position of 3 billion USDT with a leverage of 10X would require an insurance fund pay-out of [0.3 – 1/20] x 3 = 0.75 billion USDT;

- On a return of -30% a liquidated position of 3 billion USDT with a leverage of 20X would require an insurance fund pay-out of [0.3 – 1/40] x 3 = 0.825 billion USDT.

Auto-Deleveraging

If Bob does not close out a winning short position when his counterparty has been liquidated, he could be auto-deleveraged (ADL) by the exchange. Most exchanges employ a traffic light warning system about ADL, such as this one from BitMEX. Quote from BitMEX: “The Insurance Fund is used to prevent ADL. If it is depleted for a given contract, ADL will occur.” Binance’s ADL system appears to work similarly but the language is more obscure.

The point to note here is that, in contrast with liquidations, ADLs typically have a warning system. If there have been a lot of liquidations of losing positions, the winning counterparties need to close out before they get ADL’d. Thus, Bob can close his original position, with the leverage he initially chose, but if he does not close it then a gain of, say, $100,000 on a 100x leveraged position could suddenly be cut to $10,000 if his position is ADL’d to 10X.

In March 2021 Binance issued a guarantee of no ADL, provided the notional traded on some major products was less than 4 billion USDT. On 18 April the trading volume got pretty close to 4 billion USDT. The threat that the no-ADL guarantee could be revoked on 19 May is one reason why professional traders on Binance would want to close out winning short positions quickly. As it was, the outage of the platform killed trading volumes that day anyway, so once the platform re-opened the ADL guarantee still held. Besides, the price had recovered to previous levels by then and unrealised gains made on short positions had disappeared.

Historical Data on the Insurance Fund

According to the Binance website here, “Binance has self-funded the majority of its insurance fund, which has steadily grown by 15% from its initial 10 million USDT.”

Historical data on the insurance fund for each product are available to view but not to download. Viewing these, you’ll see that the insurance fund on almost every product follows an almost linear upwards trend. For instance, the BTCUSDT futures insurance fund currently has USDT 390m, a rise of 75% since the beginning of this year. One insurance fund covers many products, but this is not stated anywhere on the Binance website. Nevertheless, the evidence seems clear, as follows.

By laboriously looking into the history of each insurance fund here and comparing them product by product I find several funds have identical histories. For instance, the BTCUSDT fund value is currently 393,114,364.75 USDT and the ETH USDT fund has exactly the same value – the two funds also have identical histories. Similarly, DASH, ZEC, ATOM and several other coins have identical historic fund values (currently about 240 million) and XRP, EOS, LTC, LINK, ADA, and a bunch of other coins also appear to share the same fund, currently valued at about 163 million. Likewise for minor coins, these all seem to share the same fund, with current value about 11 million.

It seems that there are actually three main funds in Binance’s aggregate insurance fund – the fund for BTC/ETH, the fund for DASH/ZEC/ATOM/…, and the fund for XRP/EOS/LTC/LINK/ADA/…. On 19 May 2021 the aggregate value of these funds was about 650 million USDT, of which 632.7 million USDT was allocated to three largest funds as follows:

Insurance Fund Value on 19 May Value on 20 May

- BTC/ETH: 291,853,183 USDT 288,718,799 USDT

- DASH/ZEC/ATOM/...: 195,026,688 USDT 194,767,999 USDT

- XRP/EOS/LTC/LINK/ADA/...: 145,825,533 USDT 145,763,166 USDT

Taking the difference between the column sums, the three largest funds together fell by only 0.5%, that is by 3,455,440 USDT between 19 and 20 May. t is a difficult job to examine funds on several hundred different products – the exercise requires data scraping and then conversion of historical coin margined fund values into USDT at the prevailing rate. The only information I can find about the aggregate value of their fund is from Binance’s press reports. For instance, back in March 2020 this report shows the BTCUSDT fund halved from 12 million to 6 million. Again, on 11 May 2020 Binance accepted that 13 million USDT of “the” insurance fund was used to mitigate ADLs. The BTC/ETH USDT fund dropped from 21 to 7.7 million on 11 May 2020.

After this, Binance reported adding 30 million USDT to “the fund” and the BTC/ETH USDT fund rose by about 25 million. The XRP et al. fund rose by 2 million USDT and the DASH et al. fund rose by 1 million. I assume the remaining 2 million (1/15th of the 30 million reported) was added to the residual funds covering minor products. The allocation of the aggregate fund seems to be roughly proportional to trading volume: the BTC/ETH fund takes the lion’s share, and the other two funds listed above take up most of the rest. Given the press reports, I assume the funds I haven’t examined on the Binance website only take up about 1/15th of the total insurance fund value. So, my best estimate of the aggregate value of the insurance fund at the time of writing is 390 + 240 + 163 + 11 = 804 million USDT plus 1/15th for products I haven’t examined, making a total aggregate fund value of about 850 million USDT, compared with about 650 million USDT on 19 May. The purpose of the insurance fund is to pay the winning counterparties of liquidated positions. Given the reported liquidations shown in Figure 5 it is, therefore, very strange that value of the insurance fund hardly ever decreases. For instance, 50% of open interest was liquidated on 18 April, yet apparently the BTC/ETH USDT fund value grew by about 9 million USDT (from 217 to 226 million USDT) between 18 and 19 April.

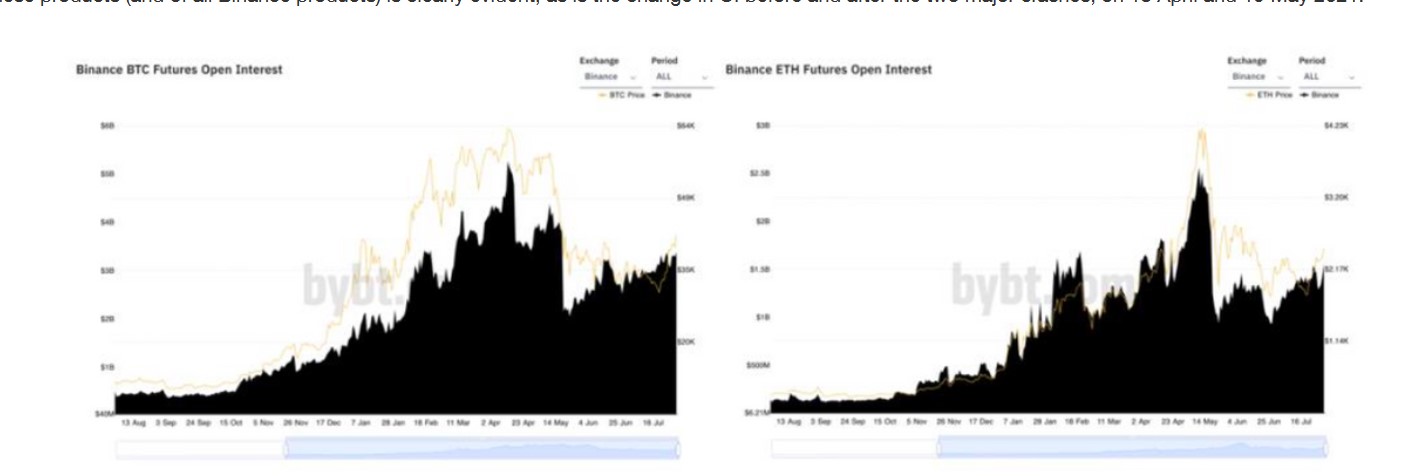

Open Interest

Recall from Figure 5 that 50% of the pen Interest (OI) on the BTCUSDT perpetual was liquidated on 18 April. I haven’t downloaded the data but liquidations as a percentage of OI are likely to be similar on the other BTC and ETH futures. Bybit provide data for OI relevant to the BTC/ETH insurance fund which covers all BTC and ETH futures. Figure 9 depicts the evolution of the open interest on BTC (left) and ETH (right) over the last 12 months. The rapid growth in these products (and of all Binance products) is clearly evident, as is the change in OI before and after the two major crashes, on 18 April and 19 May 2021.

Estimations of Insurance Fund Pay-Outs

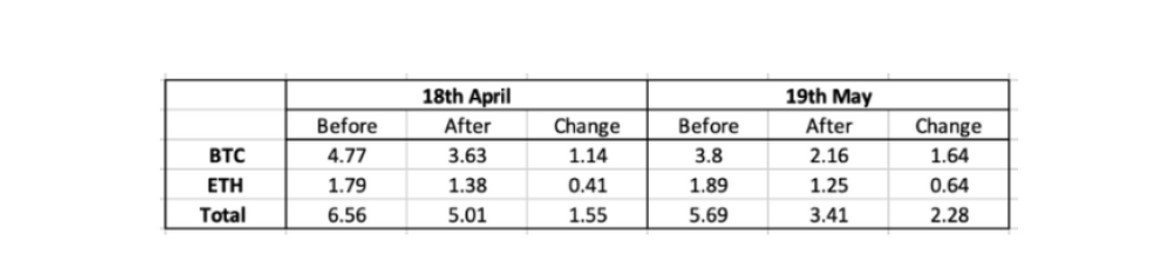

To apply the formula for the insurance fund pay-out, for a given return on a certain notional, one can observe the return and one can estimate the notional using data on OI and percentage of liquidations. The value N is obtained by assuming 50% of OI was liquidated on all three funds on 19 May, as we know it was on 18 April. From Table 1 above, this gives N = 0.5 x 6.36 = 3.18 billion USDT for 18 April and N = o,5 x 5.69 = 2.845 billion USDT on 19 May. Again, this is just for the BTC/ETH fund, whose value was 217,677,124.28 USDT on 18 April and 291,853,183 USDT on 19 May.

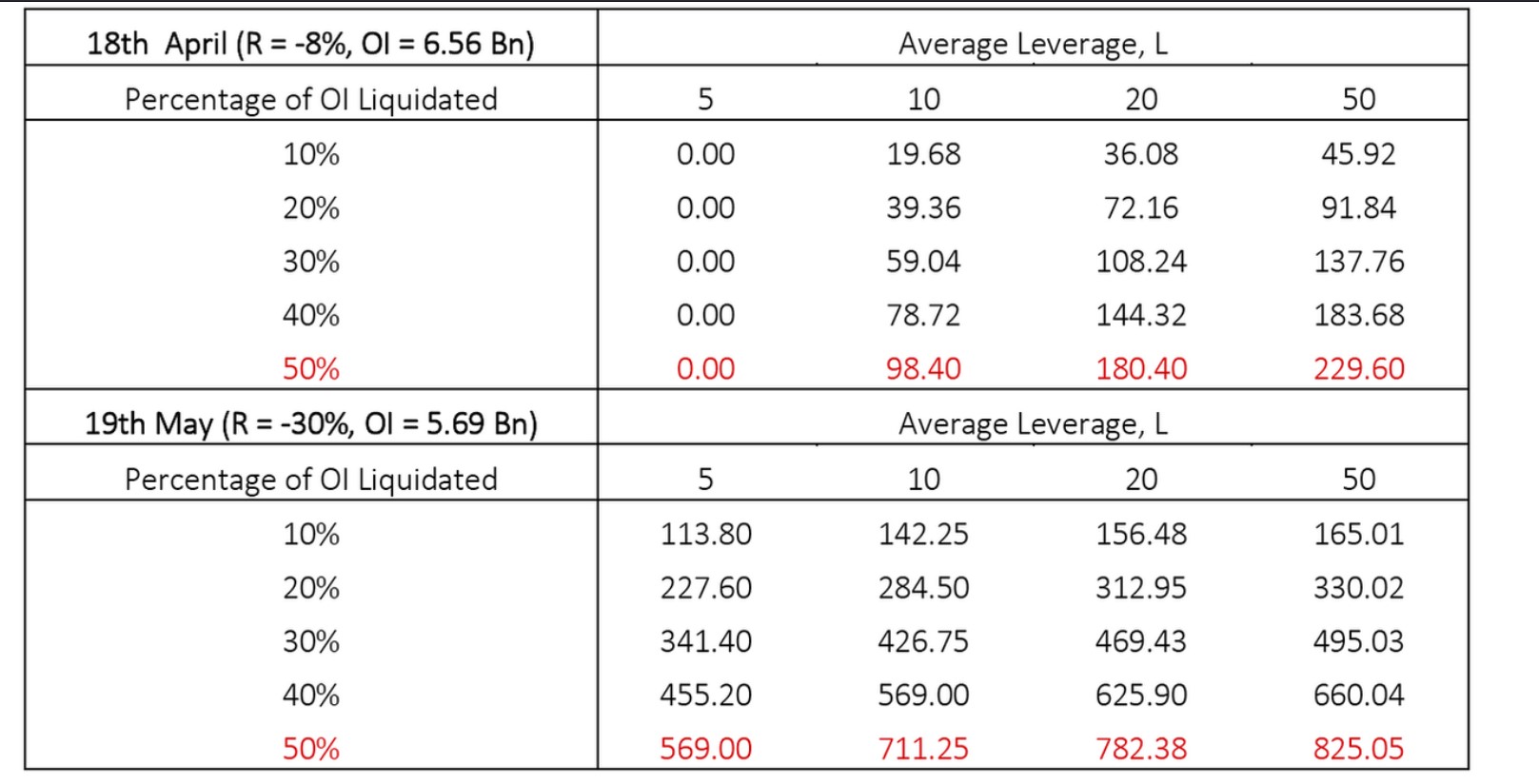

Next, we need to estimate an average leverage L in our formula for insurance fund pay-outs. On 26 July Binance announced a new leverage limit of 20X, whereas previous it had been up to 100X, or even 125X on the inverse futures products. Interestingly, 20X is also the average implied leverage calculated in my forthcoming paper Alexander, Deng and Zou (2021) “Liquidations of Perpetuals, Speculation Indices and Optimal Hedging of Bitcoin”. Table 2 reports my estimates of BTC/ETH insurance fund pay-outs on 18 April and 19 May, under different scenarios for average leverage. On 18 April we know that about 50% of OI was liquidated. Since no insurance pay-out was recorded, either no winning counterparties took their gains, or the leverage was very low (less than 7%), or the insurance fund data are inaccurate. But on 19 May, even if we assume average leverage was only 5%, the BTC/ETH would have had to pay out 569 million USDT, assuming that again 50% of OI was liquidated. The fund value on 19 May was a little under 292 million USDT, which is insufficient to cover a 569 million USDT claim.

Even on conservative estimates, say only 30% of OI was liquidated on 19 May, if the average leverage was just 5X on the BTC/ETH products, the potential claim on the fund (if the winning positions were able to close) was 341.4 million USDT, which is nearly 50 million USDT more than the fund value. At 20X leverage, and with 50% of OI being liquidated, if the platform had not gone down the potential claim would have been 782.38 million USDT – i.e. almost ½ billion more than the fund’s value. Since there are two other major funds to consider as well, we are looking at potential claims of well over 1 billion USDT on 19 May, if the winning counterparties to liquidated positions had been able to realise their profits. But the platform went down, so they couldn’t close their positions.

Toxic Flow

Toxic flow is a term used by professional traders OTC desks, hedge funds, high-frequency traders and other market makers. It refers to trade flow originating from informed traders who adversely select uninformed flow to their advantage. Professional traders (like Bob) are better informed than retail investors (like Alice) and they don’t like trading against another informed trader (like Eve). Bob prefers to trade with a counterparty he has an informational advantage over – like Alice, or Carol, or Dave or any other ordinary investor who doesn’t understand the market as well as Bob does.

Binance has a business model that tries to attract retail trade. To protect retail investors, regulators such as the FCA in the UK and many others globally have refused Binance subsidiaries a license to operate. Nevertheless, plenty of retail investors use Binance and for this reason it has become the preferred venue for professional traders, especially those from the US. We can see this from the volume time-of-day patterns, and the patterns of volatility transmission which are greatest during the opening hours of US markets. See Alexander, Heck and Kaeck (2021) “The Role of Binance in Volatility Transmission” for more information. The reason why professional traders like Binance, is that their business model attracts little fish (Alice, Carol, Dave…) for the big fish like Bob and Eve to feed off. It does this by providing all sorts of educational videos which aim to assure retail investors of the safety they have when trading on Binance, translated by unpaid Binance fans called ‘Angels’.

Tether and the US Bill

Tether's usage has been precipitated by demand from Binance because it is almost impossible to transfer fiat currency on and off the exchange and tether is the obvious choice for U.S. traders. For instance, Paolo Ardoini, CTO of Tether and Bitfinex, tweeted that Binance ordered $3bn more tether to be minted specifically for Binance, and the tether rich list attributes 20-30% of tether coins to one of Binance’s cold wallets the amount having fallen considerably since May 31 when the supply of tether stopped. The time-of-day patterns in volume and volatility flows that Alexander, Heck and Kaeck (2021) uncover, taken together with the Binance fee structure (which rewards large trades), the pegging of tether to the U.S. dollar, the rapid and simultaneous growth in both tether market cap and Binance traded volumes since July 2020 (which is when U.S. banks were first permitted custody of crypto assets) all point to the volatility transmission from the Binance tether perpetual emanating from U.S. professional traders.

Binance may also be implicated in the long-standing concerns about tether's collateralization. The stable coin’s issuer, Tether Limited, originally claimed to hold one U.S. dollar for each token of tether. But in May 2021, after recurring accusations of creating un-backed tokens and a prolonged investigation by the New York Attorney General, Tether reported that only 2.9% of all tokens are actually backed by cash reserves and about 50% is in commercial paper, a form of unsecured debt that is normally only issued by firms with high-quality debt ratings. The simultaneous growth of Binance and tether begs the question whether Binance itself is the issuer of a large fraction of tether’s $30 billion commercial paper. Binance's B2B platform is the main online broker for tether. Suppose Binance is in financial difficulties (possibly precipitated by using its own money rather than insurance funds to cover payment to counterparties of liquidated positions). Then the tether it orders and gives to customers might not be paid for with dollars, or bitcoin or any other form of cash, but rather with an IOU. That is, commerical paper on which it pays tether interest, until the term of the loan expires. No new tether has been issued since Binance's order of $3 billion was made highly visible to the public on 31 May. Maybe this is because Tether's next audit is imminent, and the auditers may one day investigate the identity of the issuers of the 50% (or more, now) of commercial paper it has for reserves. If it were found that the main issuer was Binance (maybe followed by FTX) then the entire crypto asset market place would have been holding itself up with its own bootstraps! Imagine a market where retail investors are injecting fiat currency -- in some cases, their entire wealth or their pension pots -- which is taken out of the system by professional traders and self-regulated financial intermediaries like Binance and Tether. To be replaced by tether, a digital asset with no real value because it is backed by worthless commercial paper. While the speculation surrounding the issuers of the commercial paper will continue as long as Tether remains unwilling to undergo a reliable third-party audit, it is definite that both Tether and Binance require more attention from regulators during the forthcoming debates on the 58-page draft bill for a new Digital Asset Market Structure and Investor Protection Act.

3 August 2021

Many thanks to David Twomey and Andrew Mann of Coinstrats for providing the Binance websocket data, making graphs, and for some very helpful comments. Thanks also to Dr. Xi Chen at Sussex for drawing the Matlab Figure 7. All errors are my own.

Search by keyword: Binance Insurance Fund: Fraud with the shutdown of the futures platform on May 19 (technical analysis and evidence)

All rights reserved © ScamBinance.com (2019-2023)

Binance scam counteraction community: The fraud of the official exchanges binance.com (binance dex, binance coin), real reviews of the fake financial website, a collection of compromising Binance fraud data. Investigation of criminal, financial, illegal, unlawful actions of the management of the toxic Binance cryptocurrency exchange: deception of traders, manipulation on the stock exchange, listings, problems of the exchange, money laundering, complaints to international regulatory authorities and law enforcement agencies on the fact of fraudulent actions of the Binance cryptocurrency exchange. The "dark legal side" of cooperation with Binance – data on the affiliates of the Binance website.